From September 16 to November 25, 2020, Professor Yunbi An of the Business Department at the University of Windsor, Canada, taught the students enrolled in master’s degree programs of the School of Finance and the School of Information in 2020 “Asset Pricing and Risk Management” online. This program was supported by the “Talent Introduction Project of the Central University of Finance and Economics.”

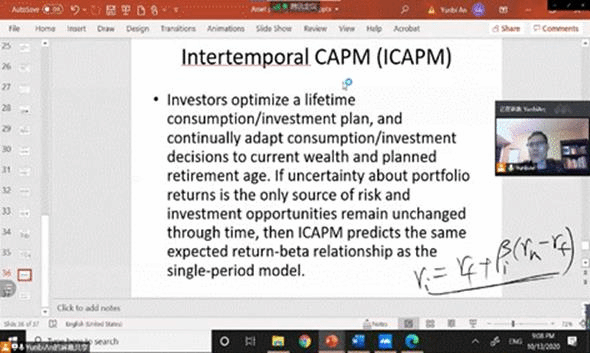

During teaching, Professor An vividly introduced the concepts, connotations, classical theories, and frontier views of modern asset pricing and risk management to the students and demonstrated how to develop the classical Capital Asset Pricing Model (CAPM) and the Arbitrage Pricing Theory (APT) Model through mathematical models and theoretical derivations alongside the inevitable expansion of relevant knowledge. He also explained modern risk management techniques in depth and detail.

Teaching

In addition, Professor An organized a paper review and a case study for the students during the course. During the paper review, the students had a thorough discussion with Professor An and analyzed deeply into the high-quality paper entitled “International portfolio selection with exchange rate risk: A behavioral portfolio theory perspective” he had published in the Journal of Banking & Finance, allowing them to gain a basic understanding of how to apply the asset pricing theory to cutting-edge academic research and how to read academic papers critically. In the case study of “Acpana Business Systems Inc.: Effect of Currency Exposure on Revenue,” Professor An invited the students to design hedging strategies for a historical scenario to manage foreign exchange risks, which considerably deepened their understanding of derivatives in the foreign exchange market and enabled them to know the calculation methods in connection with the design of hedging strategies using foreign exchange derivatives while guiding them to think more profound over the rationality of hedging strategies.

During the lecture, the master’s degree programs students attended classes actively and timely, had heated discussions on the theories after class, and carefully studied and prepared the analysis reports. When the course was near its end, Professor An organized a Q&A session for the students and patiently answered their questions about the study, life, and job applications.

Q&A session

Q&A and discussion in WeChat group after class

Professor An spoke highly of the student’s performance in the course. With the help and guidance of Professor An, the students enriched their knowledge in the field of asset pricing and risk management, improved their abilities to conduct academic research and solve practical financial problems, and enhanced their comprehensive quality.